Swimming in oil

Rust never sleeps

-Neil Young

Greetings

The tight oil "revolution", has spawned a lot of optimistic stories. These stories are unfortunately creating a false sense of security with respect to the oil situation, and the need to address our complete dependency on oil for transportation and agriculture. Also inflated idea about the future of gas, has implications for local industry, as well as our ability to close coal plants in favor of natural gas.

It is widely known that were it not for the US tight oil production, the world production of oil would have already peaked. Therefore, the question of how long the tight oil revolution will continue is very significant.

The PCI projections are much less optimistic than the standard story put out by the industry and EIA. . These graphs from peakoilbarrel, tell the story:

========

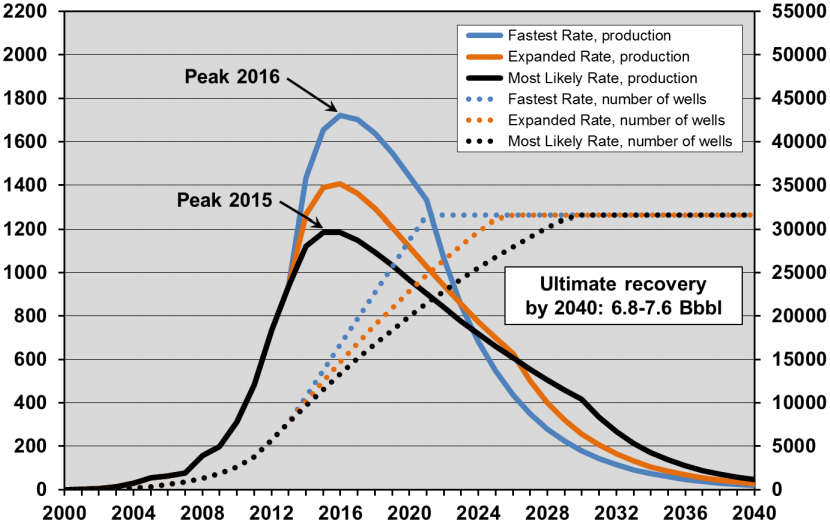

"The Post Carbon Institute’s take on things are a little different. They have the initial production a little higher than the EIA but dropping off much faster.

The Post Carbon Institute produced three cases, a Low Well Density Case, and Optimistic Case and a Realistic Case. And all three cases have three rates. In all cases the higher the initial production rate the faster the decline rate. I have posted here the Realistic Case.

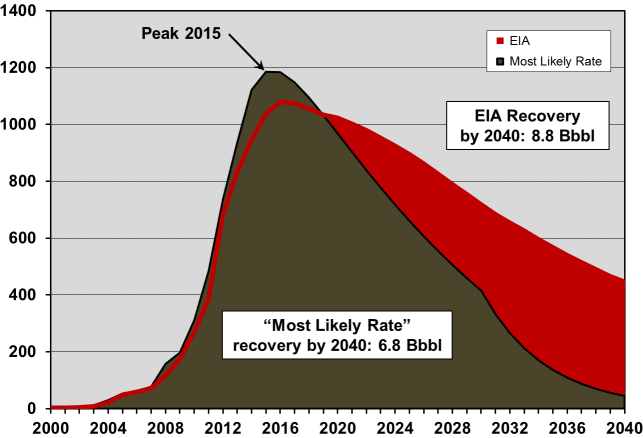

Here we can see the difference in what the EIA predits and what the PCI predicts. The EIA has production still going relatively strong by 2040 while PCI has both the Bakken and Eagle Ford petering out.

--------

Drilling Deeper: A Reality Check On U.S. Government Forecasts For a Lasting Tight Oil & Shale Gas Boom

Abstract

Abstract

Drilling Deeper reviews the twelve shale plays that account for 82% of the tight oil production and 88% of the shale gas production in the U.S. Department of Energy’s Energy Information Administration (EIA) reference case forecasts through 2040. It utilizes all available production data for the plays analyzed, and assesses historical production, well- and field-decline rates, available drilling locations, and well-quality trends for each play, as well as counties within plays. Projections of future production rates are then made based on forecast drilling rates (and, by implication, capital expenditures). Tight oil (shale oil) and shale gas production is found to be unsustainable in the medium- and longer-term at the rates forecast by the EIA, which are extremely optimistic.

This report finds that tight oil production from major plays will peak before 2020. Barring major new discoveries on the scale of the Bakken or Eagle Ford, production will be far below the EIA’s forecast by 2040. Tight oil production from the two top plays, the Bakken and Eagle Ford, will underperform the EIA’s reference case oil recovery by 28% from 2013 to 2040, and more of this production will be front-loaded than the EIA estimates. By 2040, production rates from the Bakken and Eagle Ford will be less than a tenth of that projected by the EIA. Tight oil production forecast by the EIA from plays other than the Bakken and Eagle Ford is in most cases highly optimistic and unlikely to be realized at the medium- and long-term rates projected.

Shale gas production from the top seven plays will also likely peak before 2020. Barring major new discoveries on the scale of the Marcellus, production will be far below the EIA’s forecast by 2040. Shale gas production from the top seven plays will underperform the EIA’s reference case forecast by 39% from 2014 to 2040, and more of this production will be front-loaded than the EIA estimates. By 2040, production rates from these plays will be about one-third that of the EIA forecast. Production from shale gas plays other than the top seven will need to be four times that estimated by the EIA in order to meet its reference case forecast.

Over the short term, U.S. production of both shale gas and tight oil is projected to be robust-but a thorough review of production data from the major plays indicates that this will not be sustainable in the long term. These findings have clear implications for medium and long term supply, and hence current domestic and foreign policy discussions, which generally assume decades of U.S. oil and gas abundance.

posted by Walter @ 9:59 AM

0 Comments

![]()

0 Comments:

Post a Comment

Subscribe to Post Comments [Atom]

<< Home