We've always relied on the kindness of strangers

Greetings peaksters

For a country like the US, that imports 60% of its oil, the key issue is not so much "peak oil" but "peak exports" Unfortunately many of the producers we rely on are moving from the status of exporter to importer, both because their prodcution is stagnating, but more importantly becasue they are using more at home. One reason for this is that exporting countries generally subsidize oil use by their citizens.

"Most net exporting nations subsidize domestic consumption by setting prices well below the global market price. When the price for a gallon of gas climbed to $3.32 in San Francisco, the price in Riyadh, Saudi Arabia was 45 cents per gallon, and the price in Tehran, Iran was only 33 cents per gallon (both figures are adjusted to account for differences in purchasing power parity).Consequently, as the price of oil rises, net exporters enjoy a significant boost to export incomes. In turn, rising export incomes support a variety of domestic investments which create jobs and increase domestic demand for energy and fuel. As a case in point, the average price for a barrel of oil was roughly $50 in 2005 and $100 in 2008. The doubling of price increased Saudi Arabia’s export earnings by nearly $400 million per day, and domestic oil consumption grew by 27 percent."http://theseventhfold.com/2010/04/07/breaking-news-net-oil-exports-peaked-in-2006/

Because of these subsidized prices, consumers in oil importing countries are in essence "outbid" by consumers within the oil producing country. This unpleasant fact may be hidden by world oil production figures which focus of gross oil output. Thus, while it appears that world oil production is on an "undulating plateau", oil available for export is declining.

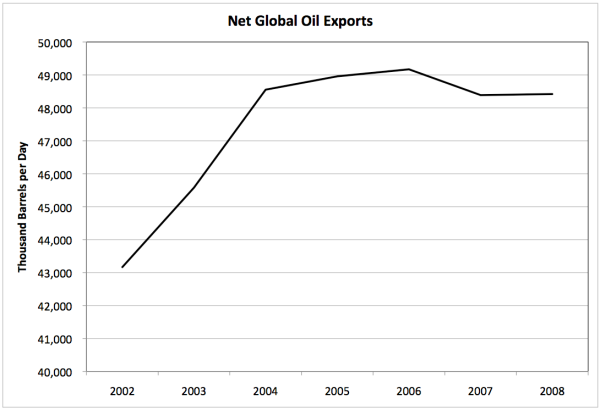

In fact it appears that "peak exports" may have already occurred

Note that in 2008, gross world oil production made a new high, but exports still declined. Oil prodcuers satisfied demand at home first, the exported what was left. Since the recession, both production and exports have fallen off, but exports have fallen faster. In 2009 production decreased by 2.6%, while exports decreased _ by 20% more_ - by 3.1% ) (see BP statistical review 2010)

Thus consumers in oil importing countries are left with a shrinking pie to fight over. The Chinese are the second largest importer of oil, and have shown that they grasp this situation, and are making,numerous deals to lock up some of this exportable oil through long term contracts. http://www.eia.doe.gov/cabs/

But what about the US? What does the future hold? It's pretty hard to tell, but it is worth taking a look at a couple of scenarios. One blog has taken a look at some possibilities. They look at the current top ten importers to the US (amounting to 85% of total US imports), and analyze likely scenarios for them.

The most likely scenario is a yearly decline of 3-4%.

"According to the prediction curve, by 2013, consumption will be about 80% of the 2005 peak, and by 2021, about 60% of the 2005 peak".

"Over the next twenty years, net exports from several of the top ten import sources is predicted to go to zero for: Mexico (2014), Venezuela (2022), Saudi Arabia and Russia (both 2023), Angola (2024), and Algeria (2030). A small amount of exports still comes from Nigeria until 2039, when its exports are also predicted to go to zero."

There is also an optimistic scenario that has only a gentle decline of 1% per year (but it requires heroic measures by Mexico, Saudia Arabia and Iraq) The most pessimistic has a decline rate of 4-5%; These scenarios are limited as they assume that the US will continue to use the current suppliers, even as they have less to offer. You can make your own assumptions about whether the US consumer would be able to outbid other players in the oil market such as China, India and the EU. While none of these scenarios are perfect, they may be useful to bracket the likely future

So, is it a big deal? One is tempted to say that the US went through a similar transition in 1978 to 1982 when consumption dropped 19% or 3.75% a year. However, it is also true that in that experience we picked the low hanging fruit - that is we transitioned a large portion oil use to natural gas. Next time won't be as easy.

It is also probably worth remembering that in the "real world" things may not follow a smooth curve. Oil is a necessity of modern life, like food and water. And like food and water, people will not agree to give them up easily.

It may be worth considering Dmiti Orlov's views on how this will play out.

"...it becomes difficult to imagine that global oil production could gently waft down from lofty heights in a graceful smooth and continuous curve spanning decades. Rather, the picture that presents itself is one of stepwise declines happening in more and more places, and eventually encompassing the entire planet. Whoever you are, and wherever you are, you are likely to experience this as a three-stage process:

Stage 1: You have your current level access to transportation fuels and services

Stage 2: You have severely limited access to transportation fuels and services

Stage 3: You have no access to transportation fuels and severely restricted transportation options

How long Stage 2 will last will vary from one place to another. Some places may go directly to Stage 3: gasoline tankers stop coming to your town, all the local gas stations close, and that is that. In other places, a thriving black market may give you some access to gasoline for a few years longer, at prices that will allow some uses, such as running an electrical generator at an emergency center. But your ability to successfully cope with Stage 2, and to survive Stage 3, will be determined largely by the changes and preparations you are able to make during Stage 1.

It should be expected that the vast majority of people will have done nothing to prepare, remaining quite unaware of the fact that this is something they should have been doing. Quite a few people can be expected to take a few small steps in a sensible direction, such as installing a wood stove, or insulating their home, or in a seemingly sensible but ultimately unhelpful direction, such as wasting their money on a new hybrid car or wasting their energies on trying to form a new political party or to lobby one of the existing ones. Some will buy a homestead, equip it for life off the grid, start growing all their own food (perhaps transporting their perishable surplus to a nearby farmer's market by cargo bicycle or by boat), and home-school their children, putting an emphasis on the classics and on agriculture, animal husbandry and other perennially useful knowledge. Some will flee to a place where transportation fuels are scarce already, and where a moped is considered a labor-saving device -- for your donkey or camel.

Unfortunately, it is hard to foresee which changes and adaptations will succeed and which will fail, because so much depends on the circumstances, which are sure to be unpredictable and vary from place to place, and on the person or persons involved: the uncertainty is just too great. But there is one thing of which we can be quite sure: that Peak Oil's Rosy Scenario, which projects a long and gradual global oil production decline, is bunk. Knowing this fact should impart a sense of urgency. Whether we use that sense of urgency foolishly or wisely is up to us, and our success may be a matter of luck, but having a sense of urgency is not at all bad. If we wish to prepare, we most likely have a few months, we may have a few years, but we certainly do not have a few decades. Let those who would have you believe otherwise first consider the issues I have raised in this article."

posted by Walter @ 4:48 PM

0 Comments

![]()

0 Comments:

Post a Comment

Subscribe to Post Comments [Atom]

<< Home